Important information: The value of investments and any income derived from them may go down as well as up. You may not get back the amount originally invested. Past performance is not a reliable indicator of future results.

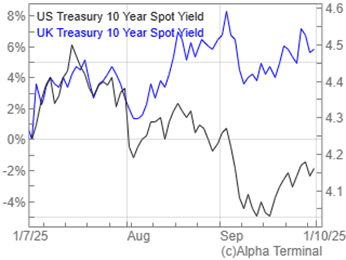

DIVERGING CENTRAL BANK STRATEGIES+

• The trajectory of interest rates around the world have diverged as the Fed cut rates to 4.25%, whilst the Bank of England and European Central Bank held at 4% and 2% respectively.

• Persistent inflation in the UK, driven largely by higher food and services costs is the main cause of rates remaining higher in the UK.

• The direction of interest rates, and inflation, coupled with difficult decisions ahead for the UK Government has caused the yield on US and UK Government Bonds to drastically separate.

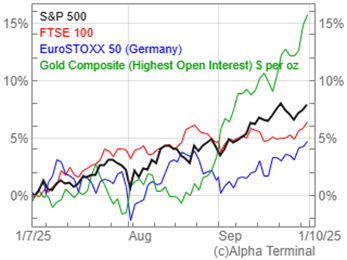

CONFLICTING MARKET SIGNALS+

• Global equity indices reached new record highs in Q3, reflecting investor optimism in corporate earnings and economic resilience.

• Safe-haven assets told a different story. The Gold price has risen above US$4,000 per ounce, a staggering record high. These are signals usually associated with caution and risk aversion.

• The coexistence of record equity markets and elevated demand for defensive assets highlights the unusual bifurcation in sentiment; markets are pricing both confidence and concern simultaneously, without a clear prevailing narrative.

AN OPPORTUNITY FOR ALTERNATIVES TO SHINE+

• Conflicting market signals, ongoing geopolitical risks, and unpredictable monetary and fiscal policy underscore the importance of Alternatives in a portfolio.

• These include those spanning infrastructure, commodities, property, private equity and structured products — and provide return streams less correlated with traditional markets.

• Their role is not to shoot the lights out, but to stabilise portfolios in times of market stress.

• The chart above shows how Infrastructure and Commodities performed vs US Equities and Global Bonds in a risk-off environment (2022).