Important information: The value of investments and any income derived from them may go down as well as up. You may not get back the amount originally invested. Past performance is not a reliable indicator of future results.

The following charts illustrate Bowmore's outlook for markets in Q1 2026. Use the tabs to navigate for quick, scroll-friendly insights.

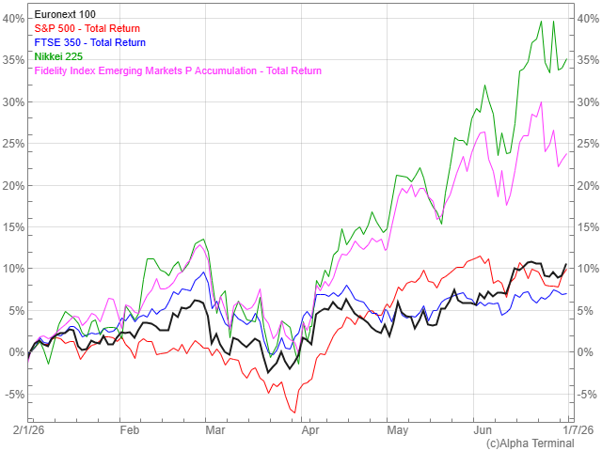

EM and Japan paving the way+

Source: Alpha Terminal, July 2026. Note the Fidelity Index Emerging Markets fund aims to track the performance of the MSCI Emerging Markets index before fees and expenses are applied.

• In the first half of 2026, Japan and Emerging Markets dominated the other major indices with respect to share price returns. Japan closed H1 up 35%, the Emerging Markets index was up just shy of 25%, while Europe and the US delivered between 10 and 11%, and the UK just 7%.

• Why have Japan and Emerging Markets done so well? One factor behind the strong performance appears to be investor demand for semiconductor and AI-related companies, particularly in markets where valuations were lower than comparable US stocks, effectively providing AI exposure at a discount.

• 40% of the value of the Japanese index, the Nikkei 225, is in semiconductors and technology hardware.2 The top 3 holdings in the EM index (which make up almost 30% of it) are TSMC, Samsung and SK Hynix – all semiconductor and/or tech companies.3

• With US corporates sitting above the 90th percentile of ‘expensiveness’ at the start of the year, the regional rotation to find AI stocks at a more reasonable price was consistent with our broader valuation-based investment approach.

• Bowmore portfolios have maintained an underweight to the US and overweight to both Japan and EM throughout the year, which has supported portfolio performance this year.

1Alpha Terminal

2Japan’s Market is Booming – Stansberry Research

3Fidelity Index EM Factsheet

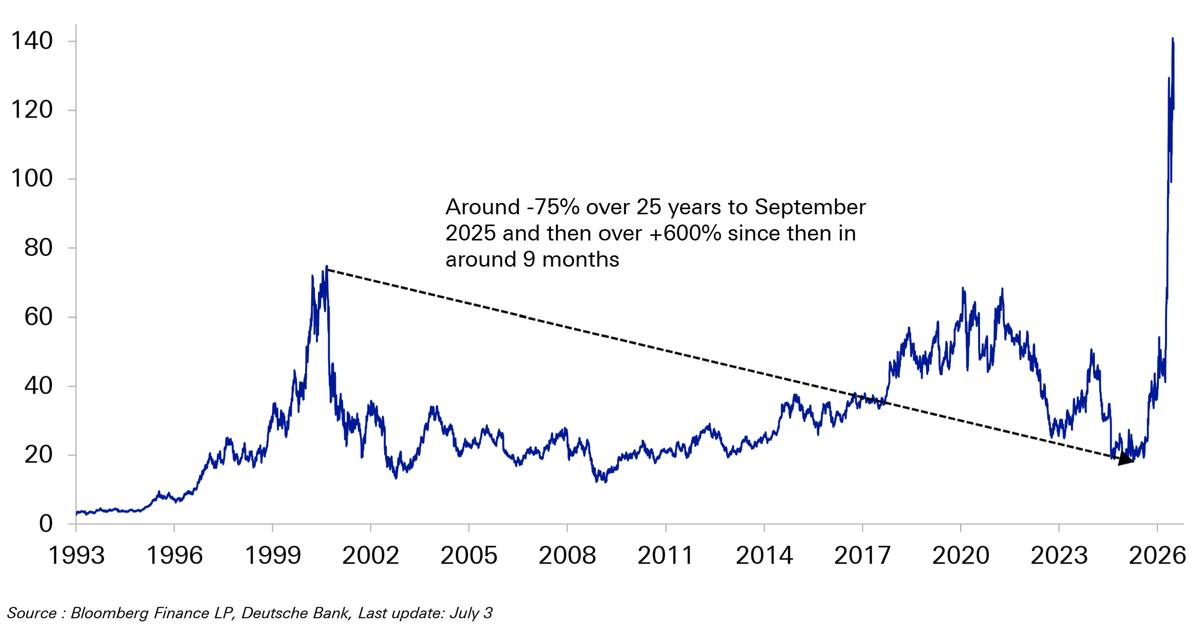

A lesson from Intel+

Source: Bloomberg Finance LP, Dautche Bank, Last Update: July 3

• The chart above shows Intel’s share price over the last 33 years. As Deutsche Bank explains, from its peak in 2000, a shareholding in Intel would be down approximately 75% over the last 25 years to September 2025. However, in the last 10 months, it has skyrocketed past its previous peak.

• This is not a lesson on patience, but rather a warning that when valuations get too stretched and break it can take a long time to recover losses. If you were to look at a chart of the South Korean stock market, the KOSPI, over the last 18 years, you would notice similarities with Intel. It did almost nothing for 17 years, and then went parabolic over the last year, with the index tripling, and becoming a larger stock market than the UK, France and Germany.4

• Meanwhile, KOSPI earnings have not just kept up, but have actually outpaced the large share price moves. Due to the huge earnings growth within SK Hynix and Samsung, the South Korean stock market still trades at almost a 70% discount to the US.4 While we think there is still some wind in the sails, we are cautious that expectations on these semiconductor stocks are astronomical – and markets hate to be disappointed.

4Deutsche Bank – Charts to make you go WOW

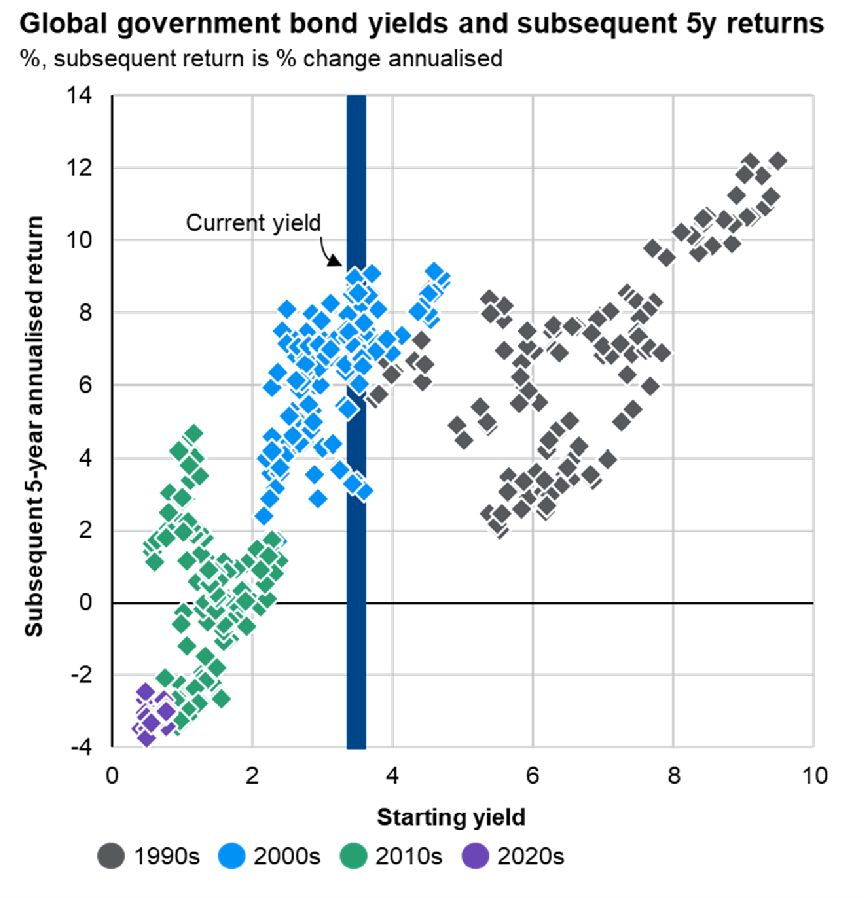

THE 2026 POTHOLES+

Source: JPMorgan Guide to the Markets, July 2026

• It would be an understatement to say that Emerging Market Equities surpassed our expectations this year. On the back of this exceptional run, we have recently taken profits on one of our EM funds, Lazard Emerging Markets. The fund has performed very strongly during our holding period. It is worth noting we still have exposure to the region but have reined in our overweight.

• We have recycled the proceeds of this into a Gilt (UK Government bond). These lower-risk investments offer a compelling yield, just shy of 4%, but also have the opportunity to achieve capital growth as interest rates come down.

• JPMorgan’s chart above highlights how, at the current starting yield of less than 4%, future annualised returns have been in the 6-8% range, although future returns are not guaranteed. This is central to our de-risking. With valuations and earnings expectations where they are in both the US and EM, we don’t forecast a recession, our base case is for more modest equity market returns than those experienced recently.

• If we can get an equivalent return on a low-risk government bond (lower-risk relative to equities) with a fraction of the volatility, we don’t need to be greedy; we can be patient and wait for new opportunities to present themselves.