Important information: The value of investments and any income derived from them may go down as well as up. You may not get back the amount originally invested. Past performance is not a reliable indicator of future results.

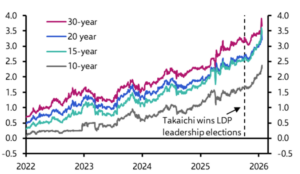

- The 30-year Japanese Government Bond (JGB) yield moved c.0.3% to a record high of 3.8% this week1

- This move followed PM Sanae Takaichi’s announcement of a further 5.8% increase in spending2

- Japan’s large cap stock market has outperformed the US, UK and Europe year to date, returning 3.4% at the time of writing1

Source: Capital Economics and London Stock Exchange Group, 2026

Affordability

While markets were quick to focus on proposed tax cuts, such as the suspension of the 8% sales tax on food and beverages, we see reassuring evidence suggesting that the sell-off at the long end of the curve may be overstated. Japan’s return to inflation (currently 2.1%³) has supported stronger nominal growth and, in turn, higher tax receipts, which are helping to reduce the debt-to-GDP ratio. JK Investments estimates that this ratio is now declining at a pace of approximately 6% per annum.

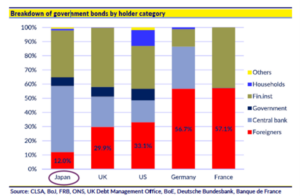

Moreover, the ownership composition of JGBs provides an additional stabilising force. The Bank of Japan holds approximately 50% of outstanding JGBs, while only around 12% are held outside the region, limiting the scope for sustained bond vigilante pressure. This stands in sharp contrast to US government debt, of which roughly $3 trillion, or about 10%⁴, is held by Europe, and 33.1% is owned by non-domestic investors⁵.

Source: Capital Economics and London Stock Exchange Group, 2026

Affordability

While markets were quick to focus on proposed tax cuts, such as the suspension of the 8% sales tax on food and beverages, we see reassuring evidence suggesting that the sell-off at the long end of the curve may be overstated. Japan’s return to inflation (currently 2.1%³) has supported stronger nominal growth and, in turn, higher tax receipts, which are helping to reduce the debt-to-GDP ratio. JK Investments estimates that this ratio is now declining at a pace of approximately 6% per annum.

Moreover, the ownership composition of JGBs provides an additional stabilising force. The Bank of Japan holds approximately 50% of outstanding JGBs, while only around 12% are held outside the region, limiting the scope for sustained bond vigilante pressure. This stands in sharp contrast to US government debt, of which roughly $3 trillion, or about 10%⁴, is held by Europe, and 33.1% is owned by non-domestic investors⁵.

Source: JK Investments, December 2025

With interest rates still well below those of other developed economies (currently 0.75%³), Japan is uniquely positioned to borrow at a comparatively low cost and deploy capital into higher-yielding global assets. In addition, the country maintains substantial public and quasi-public asset pools to support its ageing population, alongside the world’s second-largest foreign exchange reserves5.

As discussed in our previous piece on Japan, these debt dynamics further reinforce the country’s distinctive economic micro-climate and have helped to rekindle investor interest in the region.

Bowmore Portfolios

We maintain only a negligible allocation to Japanese bonds across both government and corporate issuers, instead favouring UK debt for the majority of our fixed income exposure. Currently, 57.7% of the total fixed income allocation within the Core 5 portfolio is invested in UK assets, a positioning that eliminates currency risk and reflects our expectation of further interest rate cuts this year.

Back in October 2025 however, we made a rotation within our Japanese equity exposure, shifting towards a smaller cap, more domestically focused strategy. This allocation was selected to capture the benefits of a broadening corporate governance reform agenda, strengthening wage growth, and a recovering Yen. Since its inclusion in portfolios, the fund has delivered a return of 5.92%.

Source: JK Investments, December 2025

With interest rates still well below those of other developed economies (currently 0.75%³), Japan is uniquely positioned to borrow at a comparatively low cost and deploy capital into higher-yielding global assets. In addition, the country maintains substantial public and quasi-public asset pools to support its ageing population, alongside the world’s second-largest foreign exchange reserves5.

As discussed in our previous piece on Japan, these debt dynamics further reinforce the country’s distinctive economic micro-climate and have helped to rekindle investor interest in the region.

Bowmore Portfolios

We maintain only a negligible allocation to Japanese bonds across both government and corporate issuers, instead favouring UK debt for the majority of our fixed income exposure. Currently, 57.7% of the total fixed income allocation within the Core 5 portfolio is invested in UK assets, a positioning that eliminates currency risk and reflects our expectation of further interest rate cuts this year.

Back in October 2025 however, we made a rotation within our Japanese equity exposure, shifting towards a smaller cap, more domestically focused strategy. This allocation was selected to capture the benefits of a broadening corporate governance reform agenda, strengthening wage growth, and a recovering Yen. Since its inclusion in portfolios, the fund has delivered a return of 5.92%.

Source: Alpha Terminal, data as at 29/01/2026

The value of your investments can go down as well as up, so you could get back less than you invested. Past performance is not a guide to future performance.

Sources:

1 AM Insights, 29/02/2026

2 Capital Economics, 2026

3 Trading Economics, 2026

4 Morningstar, 2026

5 JK Investments, 2026

6 Wavemaker, 2021

7 McKinsey & Co, 2017

8 CNBC, 2025

9 Reuters, 2025

10 Fortune Business Insights, 2025

Source: Alpha Terminal, data as at 29/01/2026

The value of your investments can go down as well as up, so you could get back less than you invested. Past performance is not a guide to future performance.

Sources:

1 AM Insights, 29/02/2026

2 Capital Economics, 2026

3 Trading Economics, 2026

4 Morningstar, 2026

5 JK Investments, 2026

6 Wavemaker, 2021

7 McKinsey & Co, 2017

8 CNBC, 2025

9 Reuters, 2025

10 Fortune Business Insights, 2025