- For two decades, US equity markets steadily shrank as the world's most cash-generative companies spent hundreds of billions buying back their own shares. That era is over. Market activity suggests that AI has forced a reversal.

- The listing of SpaceX is emblematic of this shift; the largest in history yet built on a valuation that many investment professionals feel requires extraordinary assumptions and carries serious structural questions.

- At Bowmore, we have been cautious on US valuations for some time. Nothing about this wave changes that view, but the fundamental strength of corporate earnings continues to support our confidence in equities overall.

From buybacks to fundraising

For more than two decades, the US stock market enjoyed a tailwind that most investors barely noticed. The talismanic technology companies, almost without exception, are cash-printing machines that need little capital to run. With limited use for their mountains of money, they consistently bought back their own shares. Large US companies spent over $1 trillion on buybacks in a single year at the peak

1. Fewer shares available, and an increasingly rabid demand to buy them, provided material support to US equity prices for the better part of a generation.

However, we believe this status quo has been upended by the remarkable expenditure of the large AI firms. The same companies are now racing to build AI infrastructure, including data centres, power generation, and semiconductor hardware. The capital requirements dwarf anything these businesses have faced before. The combined spending of Alphabet, Amazon, Meta, Microsoft and Oracle alone on this infrastructure is growing at 72% per year and is expected to reach $770 billion in 2026 alone

2. Morgan Stanley forecasts that the world's largest technology companies will spend approximately $3 trillion on data centres before the end of 2028

3.

No longer able to be funded exclusively from cash flows, fundraising has already begun at remarkable scale. Alphabet recently completed the largest equity offering in history, raising $84.75 billion in a single transaction, its first share issuance in twenty years

4. Meta, Microsoft and Amazon are reported to be weighing similar moves

5. After years of shrinking the supply of shares, America's largest companies are asking the public to fund them. J.P. Morgan estimates that over $260 billion of new equity from listed companies will come to market in 2026 alone

6.

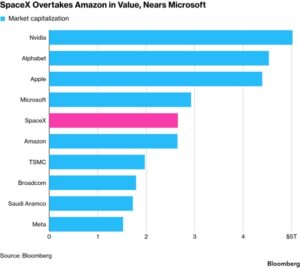

SpaceX steals the show

The most striking example of this trend debuted on the market on the 12

th of June. SpaceX raised $75 billion at a valuation of $1.77 trillion, marking the largest new listing in history

7. Within days, the stock surpassed Amazon and briefly overtook Microsoft in value

8. To be clear, this is a company that lost $4.9 billion in 2025 and $4.27 billion in just the first quarter of 2026

9,and now carries a larger market value than either of those businesses, each of which are highly profitable and decades-established.

The valuation is, in part, driven by ambitious growth expectations for its recently merged AI division, formerly known as xAI

10. Goldman Sachs has told prospective investors that AI revenues need to grow from $3.2 billion in 2025 to $322 billion by 2030 for the valuation to make sense. Total revenues would need to reach $474 billion, against $18.7 billion last year

11. However, Goldman projects negative cash flow every year through 2030, with the first profitable year in 2031

12.

The governance picture also warrants attention. Musk's Class B shares carry ten votes each against one for the public's Class A shares, giving him approximately 85% of voting rights whilst holding just 42% of the equity

13. The terms of the listing also prohibit all legal action against Musk in respect of his management of the company

14.

The share price itself has been supported in large part by structural mechanics that are worth understanding. Retail investors were allocated around 30% of the initial public offering (IPO) and their brokers imposed lock-ups preventing them from selling early

15. Index providers including Nasdaq and FTSE Russell waived their previously iron-clad rules on profitability and a one year seasoning period specifically to allow SpaceX into their indices within days of listing, forcing passive funds to buy the stock regardless of price or fundamentals

16. The combination of locked-up retail investors, forced index buying, and a tiny float has created conditions for extreme price moves that may not reflect underlying value.

SpaceX is not alone in the pipeline. Anthropic filed for IPO at a valuation of $965 billion, and OpenAI followed at approximately $852 billion – all three firms are loss-making

17.

Bowmore portfolios

We have been underweight US equities relative to the global index and our peers for some time, and this development does not change that view. High valuations remain our central concern, irrespective of the new supply.

That said, the earnings quality of the major US technology companies remains exceptional, and we are comfortable with our current exposure. In our Core Risk Profile 5, we hold approximately 7.5% in US large-cap equities and 3% directly in technology. What gives us greater pause is the growing influence of loss-making, indebted companies within major indices.

Despite having no exposure to SpaceX, but cognisant of elevated valuations in technology stocks we do have exposure to, we are considering reorienting part of our US equity allocation towards a fund focused on undervalued, highly cash-generative businesses in less fashionable, more “old economy” sectors.

Moreover, in the context of our diversified, multi-asset portfolios, the specific risks of any single market or company are substantially mitigated. The strength of corporate earnings, not just in the US but across global equity markets, continues to support our conviction in equities as we look ahead.

Source: AlphaTerminal, data as at 17/06/2026

The value of your investments can go down as well as up, so you could get back less than you invested. Past performance is not a guide to future performance.

Sources:

1 S&P Down Jones Indices

2 Epoch

3 Morgan Stanley

4 Securities & Exchange Commission

5 Financial Times

6 J. P. Morgan

7 BuiltIn

8 CNBC

9 Financial Times

10 CNBC

11 Financial Times

12 24/7 Wall Street

13 BitMEX

14 Reuters

15 Reuters

16 InvestmentNews

17 Yahoo Finance